Sample Size and Trading Expectancy

Sample size is the number of comparable trades used to evaluate a strategy. Expectancy is the average result the strategy may produce per trade over a large sample.

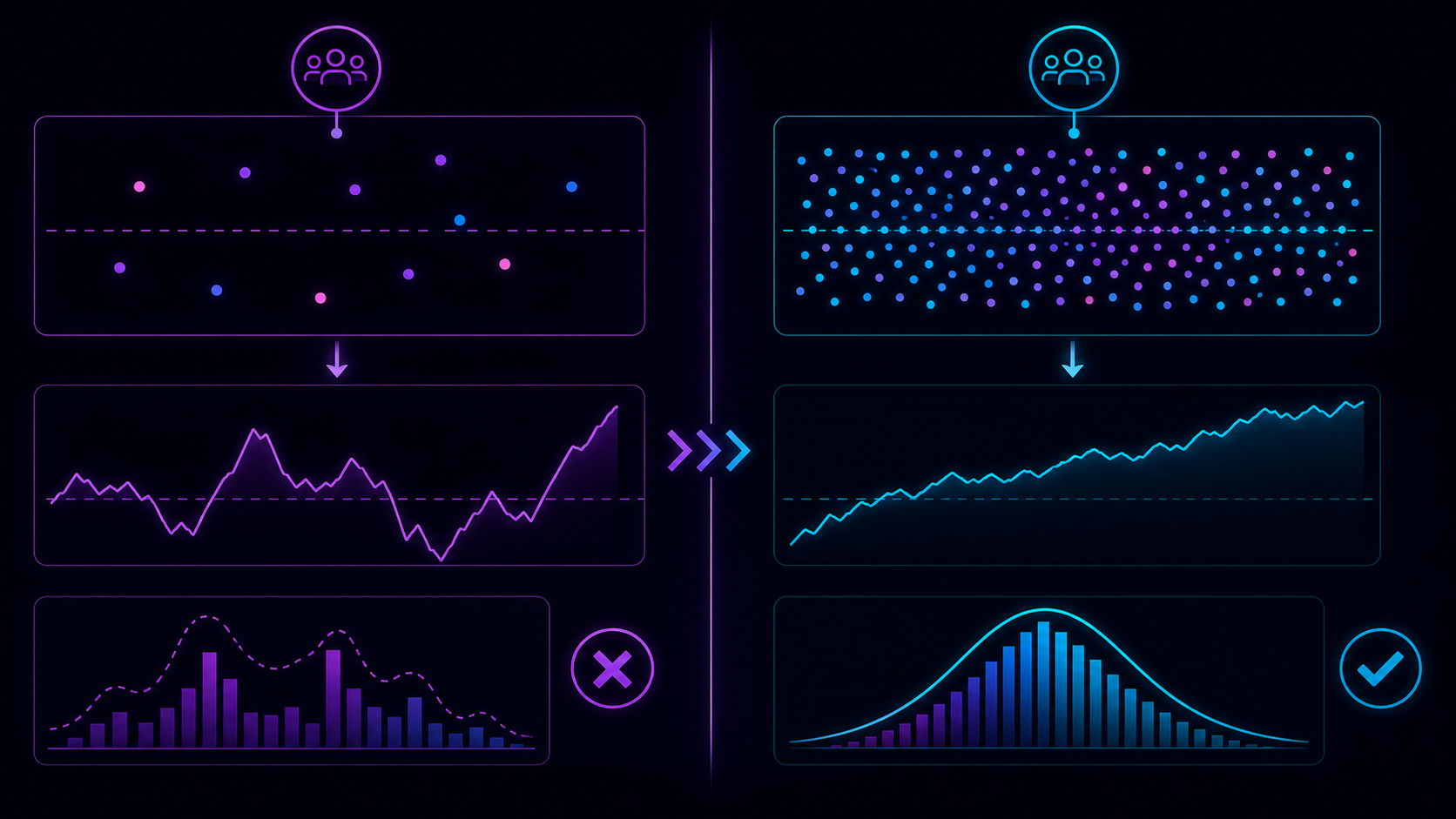

You cannot fairly judge a strategy from a few random trades, especially if those trades used different rules, indicators, timeframes, or market conditions.

Why a Few Trades Prove Almost Nothing

Three wins do not prove a strategy works. Three losses do not prove it fails.

Small samples are noisy because outcomes can cluster. A good strategy can lose several times in a row. A bad process can win several times in a row.

The question is not:

Did the last trade win?

The question is:

What happens when the same rules are applied consistently across a meaningful sample?

Comparable Trades Matter

A sample is useful only when trades are comparable.

Do not mix:

- different strategies;

- different indicator settings;

- different timeframes;

- different market regimes;

- discretionary rule changes;

- revenge trades;

- experiments and planned trades.

If the rules changed, you are starting a new sample.

Expectancy in Simple Terms

A simplified expectancy formula:

expectancy = (win rate x average win) - (loss rate x average loss)

Positive expectancy does not mean every trade wins. It means the average result may be positive over enough comparable trades.

Process Score vs PnL

Track process separately:

- Did the trade meet the setup rules?

- Was risk sized correctly?

- Was invalidation respected?

- Was the trade managed according to plan?

- Was the result logged honestly?

If process is poor, PnL is not trustworthy evidence.

Continue Learning

- Review win rate vs risk-to-reward.

- Learn why not to change strategy every day.

- Create a post-trade review.

Historical expectancy can change. A large sample improves interpretation but cannot guarantee future performance.